Which two factors are required to calculate the depreciable base of an asset

Calculation. Depreciable Base = Original Cost of Asset – Salvage Value of Asset.Explanation. There are two factors that influence the calculation of an asset’s base for depreciation: the historical (original) cost of the asset as well as its salvage value. … Example. … Related Terms.

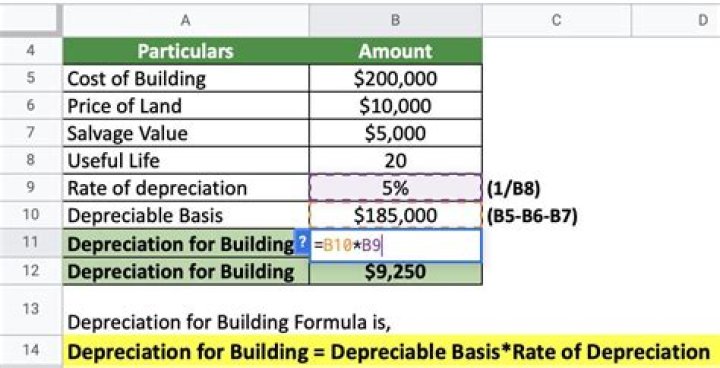

How do you find the depreciable base of an asset?

The depreciable basis is equal to the asset’s purchase price, minus any discounts, and plus any sales taxes, delivery charges, and installation fees.

What are the inputs required to calculate depreciation?

Three main inputs are required to calculate depreciation: Useful life – this is the time period over which the organisation considers the fixed asset to be productive. … This is known as the salvage value of the asset. The cost of the asset – this includes taxes, shipping, and preparation/setup expenses.

What are the factors which cause depreciation?

There are four main factors that affect the calculation of depreciation expense: asset cost, salvage value, useful life, and obsolescence.What are some of the factors that a company should consider in the selection of depreciation method?

- Legal Provisions: The statute governing an enterprise may the basis for computation of depreciation. …

- Financial Reporting: …

- Effect on Managerial Decision: …

- Inflation: …

- Technology: …

- Capital Maintenance:

Under Which method of depreciation is an asset's depreciable base the amount to be depreciated?

The correct answer is b. Under the declining-balance method, the depreciation for each period is calculated using the depreciation rate (usually double the straight-line rate) and the book value of the asset.

What is depreciation base in accounting?

Depreciation basis is the amount of a fixed asset’s cost that can be depreciated over time. This amount is the acquisition cost of an asset, minus its estimated salvage value at the end of its useful life.

What do you mean by depreciation give two reasons of decrease in the value of assets?

Assets depreciate for two main reasons: Wear and tear. For example, a car will decrease in value because of the mileage, wear on tyres, and other factors related to the use of the vehicle. … Assets also decrease in value as they are replaced by newer models.What is the depreciable value of an asset?

What Is Depreciable Value? The depreciable value of the asset is the combined cost of purchase and installation of an asset that can be depreciated minus its salvage value. For example, an asset has a cost of $20,000. At the end of its useful life, you expect to sell it off for $3000.

What is asset depreciation?Depreciation represents how much of an asset’s value has been used. Depreciating assets helps companies earn revenue from an asset while expensing a portion of its cost each year the asset is in use. Not accounting for depreciation can greatly affect a company’s profits.

Article first time published onWhat are the three factors involved in estimating the depreciation of a fixed asset?

- Useful life. This is the time period over which the company expects that the asset will be productive. …

- Salvage value. …

- Depreciation method.

What are 2 different types of depreciation?

- Straight-Line Depreciation.

- Declining Balance Depreciation.

- Sum-of-the-Years’ Digits Depreciation.

- Units of Production Depreciation.

How do you calculate depreciation under written down value method?

Depreciation for the year is the rate in percentage multiplied by the WDV at the beginning of the year. For example, for Year I – Depreciation = 10,00,000 x 12.95% i.e. 1,29,500. New WDV for subsequent year will be previous WDV minus Depreciation already charged.

What are the 3 depreciation methods?

- Straight-line method.

- Written down Value method.

- Annuity method.

- Sinking Fund method.

- Production Unit method.

What is the formula for calculating units of production depreciation?

The units of production depreciation formula is: Depreciation Expense = Unit Production Rate x Units Produced. To find the unit production rate, you must know the original value of the asset, its expected salvage value, and how many units the asset is expected to produce over its lifetime.

What is the formula for calculating straight line depreciation?

To calculate depreciation using a straight line basis, simply divide net price (purchase price less the salvage price) by the number of useful years of life the asset has.

How does depreciation affect the basis of an asset?

Whenever you claim depreciation, it reduces the tax basis of the asset in question. When you sell the asset, your gain will be equal to the sales proceeds minus the asset’s tax basis. … However, because you claimed four years of $100 annual depreciation deductions, your tax basis in the asset fell to $600.

What is depreciation explain the causes of depreciation and also the various methods of calculating depreciation?

Depreciation is a ratable reduction in the carrying amount of a fixed asset. Depreciation is intended to roughly reflect the actual consumption of the underlying asset, so that the carrying amount of the asset has been reduced to its salvage value by the time its useful life is over.

Which of the following method of depreciation provide lower amount?

Diminishing Balance Method This method is also known as reducing balance method, written down value method or declining balance method. A fixed percentage of depreciation is charged in each accounting period to the net balance of the fixed asset under this method.

How do you calculate depreciation using declining balance method?

- Straight-Line Depreciation Percent = 100% / 10 = 10%

- Depreciation Rate = 1.5 x 10% = 15%

- Depreciation for a Period = 15% x Book Value at Beginning of the Period. Depreciation for Period 1 = 15% x $575,000 = $86,250.

How do you calculate double declining balance depreciation?

Double Declining Balance Method Formula Using the Double-declining balance method, the depreciation will be: Double Declining Balance Method Formula = 2 X Cost of the asset X Depreciation rate or. Double Declining Balance Formula = 2 X Cost of the asset/Useful Life.

How do you calculate fully depreciated assets?

It is equal to the cost of the asset minus accumulated depreciation. When an asset is fully depreciated, it is worth nothing for accounting purposes, though the asset might actually have some scrap or minimal resale value.

What is depreciation and how it is calculated?

How it works: You divide the cost of an asset, minus its salvage value, over its useful life. That determines how much depreciation you deduct each year. Example: Your party business buys a bouncy castle for $10,000. Its salvage value is $500, and the asset has a useful life of 10 years.

How do you calculate annual depreciation?

Depreciation Methods in Fixed Assets The annual depreciation rate is calculated using the formula:(100 x Number of Periods In Year)/Number of periods in expected life. Each period’s depreciation amount is calculated using the formula: annual depreciation rate/ number of periods in the year.

How do you calculate depreciation on a rental property?

To calculate the annual amount of depreciation on a property, you divide the cost basis by the property’s useful life. In our example, let’s use our existing cost basis of $206,000 and divide by the GDS life span of 27.5 years. It works out to being able to deduct $7,490.91 per year or 3.6% of the loan amount.

Which of the following factors need to be known in order to calculate depreciation for a plant asset?

The factors necessary to compute depreciation include (cost/selling price/market value) (1), salvage value and useful life.

How do you calculate depreciation using the written down value method in Excel?

It uses a fixed rate to calculate the depreciation values. The DB function performs the following calculations. Fixed rate = 1 – ((salvage / cost) ^ (1 / life)) = 1 – (1000/10,000)^(1/10) = 1 – 0.7943282347 = 0.206 (rounded to 3 decimal places). Depreciation value period 1 = 10,000 * 0.206 = 2,060.00.