What is the IRS capital gains tax rate

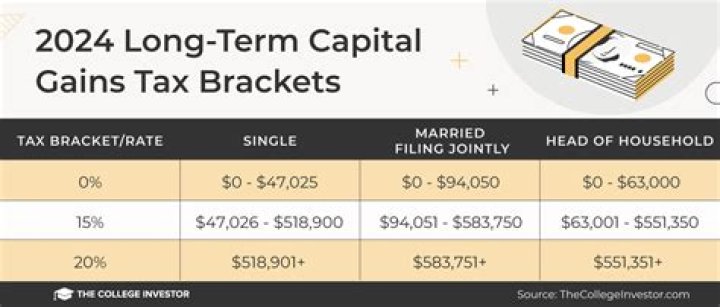

Capital Gains Tax RateTaxable Income (Single)Taxable Income (Married Filing Separate)0%Up to $40,000Up to $40,00015%$40,001 to $441,450$40,001 to $248,30020%Over $441,450Over $248,300

What is the capital gain tax for 2020?

Capital Gains Tax RateTaxable Income (Single)Taxable Income (Married Filing Separate)0%Up to $40,000Up to $40,00015%$40,001 to $441,450$40,001 to $248,30020%Over $441,450Over $248,300

Is capital gains tax 30%?

The current capital gains tax of most investments is 0%, 15%, or 20% of the profit, depending on your overall income. One big exception: If you sell the home you live in, up to $250,000 of the profit is is excluded from taxes. (It’s $500,000 for those married filing jointly.)

What is the capital gains tax rate for 2021 on real estate?

Your income and filing status make your capital gains tax rate on real estate 15%.What is the capital gains exemption for 2021?

Married investors filing jointly with taxable income of $80,800 or less ($40,400 for single filers) may pay 0% long-term capital gains levies for 2021.

Do seniors have to pay capital gains tax?

Today, anyone over the age of 55 does have to pay capital gains taxes on their home and other property sales. There are no remaining age-related capital gains exemptions. However, there are other capital gains exemptions that those over the age of 55 may qualify for.

How do you calculate capital gains tax?

In case of short-term capital gain, capital gain = final sale price – (the cost of acquisition + house improvement cost + transfer cost). In case of long-term capital gain, capital gain = final sale price – (transfer cost + indexed acquisition cost + indexed house improvement cost).

What happens if I sell my house and don't buy another?

Profit from the sale of real estate is considered a capital gain. However, if you used the house as your primary residence and meet certain other requirements, you can exempt up to $250,000 of the gain from tax ($500,000 if you’re married), regardless of whether you reinvest it.How long do you have to buy a house after selling to avoid capital gains tax?

Here’s how you can qualify for capital gains tax exemption on your primary residence: You’ve owned the home for at least two years. You’ve lived in the home for at least two years. You haven’t exempted the gains on a home sale within the last two years.

How do you avoid capital gains tax when selling an investment property?- Purchase properties using your retirement account. …

- Convert the property to a primary residence. …

- Use tax harvesting. …

- Use a 1031 tax deferred exchange.

Will capital gains change in 2021?

The maximum capital gains are taxed would also increase, from 20% to 25%. This new rate will be effective for sales that occur on or after Sept. 13, 2021, and will also apply to Qualified Dividends.

What are the 7 tax brackets?

There are seven tax brackets for most ordinary income for the 2021 tax year: 10%, 12%, 22%, 24%, 32%, 35% and 37%. Your tax bracket depends on your taxable income and your filing status: single, married filing jointly or qualifying widow(er), married filing separately and head of household.

Will tax brackets change in 2022?

Most tax brackets increase by roughly 3% from the tax year 2022. These increases to federal tax brackets are the largest increases in four years.

Is there still a one time capital gains exemption?

The exemption no longer exists as it was replaced by new rules when the Taxpayer Relief Act of 1997 was ratified into law. This act was one of the largest tax reduction acts to be put into place by the United States government.

Who qualifies for lifetime capital gains exemption?

You’re eligible for the exclusion if you have owned and used your home as your main home for a period aggregating at least two years out of the five years prior to its date of sale. You can meet the ownership and use tests during different 2-year periods.

Do you have to buy another home to avoid capital gains?

The capital gains exclusion on home sales only applies if it’s your primary residence. In order to exclude gains on sale, you would have to sell your current primary home, make your vacation home your primary home and live there for at least 2 years prior to selling.

Is capital gains added to your total income and puts you in higher tax bracket?

Your ordinary income is taxed first, at its higher relative tax rates, and long-term capital gains and dividends are taxed second, at their lower rates. So, long-term capital gains can’t push your ordinary income into a higher tax bracket, but they may push your capital gains rate into a higher tax bracket.

What is the exemption limit for long-term capital gain?

Adjustment of Long-term Capital Gain (Exemption) The exemption limit is Rs. 5,00,000 for resident individual of the age of 80 years or above. The exemption limit is Rs. 3,00,000 for resident individual of the age of 60 years or above but below 80 years.

How do I avoid capital gains tax when I retire?

- Hold onto taxable assets for the long term. …

- Make investments within tax-deferred retirement plans. …

- Utilize tax-loss harvesting. …

- Donate appreciated investments to charity.

What are the requirements to get the $250000 exemption from capital gains when you sell your home?

Here’s the most important thing you need to know: To qualify for the $250,000/$500,000 home sale exclusion, you must own and occupy the home as your principal residence for at least two years before you sell it. Your home can be a house, apartment, condominium, stock-cooperative, or mobile home fixed to land.

Do I pay capital gains if I sell my house and buy another?

When you sell a personal residence and buy another one, the IRS will not let you do a 1031 exchange. You can, however, exclude a large portion of the gain from your taxes as that you have lived in for two of the past five years in the property and used it as your primary residence.

Do I pay capital gains if I reinvest the proceeds from sale?

Capital gains generally receive a lower tax rate, depending on your tax bracket, than does ordinary income. … However, the IRS recognizes those capital gains when they occur, whether or not you reinvest them. Therefore, there are no direct tax benefits associated with reinvesting your capital gains.

How long do you have to live in your primary residence to avoid capital gains in Canada?

If you sell a cottage that you have owned for 10 years, you could designate the cottage as your principal residence for the entire 10 years in order to eliminate capital gains tax, as long as you have not designated any other property as your principal residence during that time, and as long as you have not used the …

Can you be exempt from capital gains tax?

The Internal Revenue Service allows exclusions for capital gains made on the sale of primary residences. Homeowners who meet certain conditions can exclude gains up to $250,000 for single filers and $500,000 for married couples who file jointly.

Is Social Security taxable?

Some of you have to pay federal income taxes on your Social Security benefits. between $25,000 and $34,000, you may have to pay income tax on up to 50 percent of your benefits. … more than $34,000, up to 85 percent of your benefits may be taxable.

What is the 3.8 surtax on investment income?

The net investment income tax (NIIT) is a 3.8% tax on investment income such as capital gains, dividends, and rental property income. This tax only applies to high-income taxpayers, such as single filers who make more than $200,000 and married couples who make more than $250,000, as well as certain estates and trusts.

What is the federal tax rate on 80000?

If you make $80,000 a year living in the region of California, USA, you will be taxed $22,222. That means that your net pay will be $57,778 per year, or $4,815 per month. Your average tax rate is 27.8% and your marginal tax rate is 41.1%.

Which country has the highest tax rate?

Again according to the OECD, the country with the highest national income tax rate is the Netherlands at 52 percent, more than 12 percentage points higher than the U.S. top federal individual income rate of 39.6 percent.

What is the standard deduction for 2021 over 65?

Filing StatusAdditional Standard Deduction 2021 (Per Person)Additional Standard Deduction 2022 (Per Person)Single or Head of Household • 65 or older OR blind • 65 or older AND blind$1,700 $3,400$1,750 $3,500