What are the differences between IFRS and US GAAP

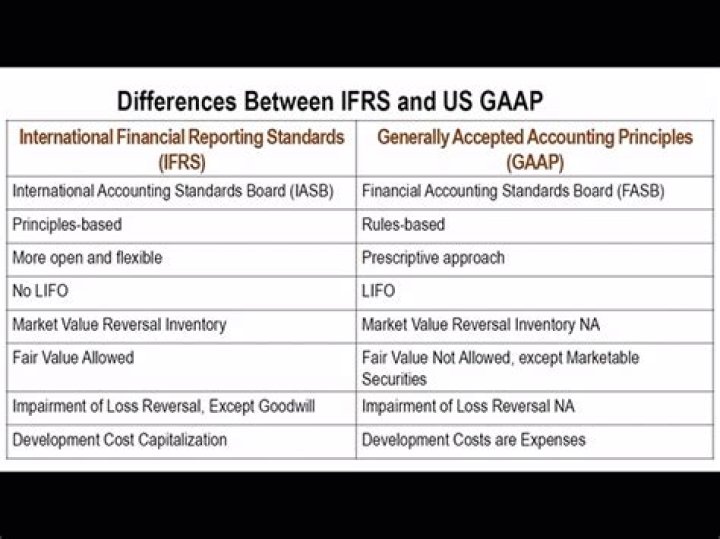

The primary difference between the two systems is that GAAP is rules-based and IFRS is principles-based. … Consequently, the theoretical framework and principles of the IFRS leave more room for interpretation and may often require lengthy disclosures on financial statements.

What are the differences between IFRS and U.S. GAAP for revenue recognition?

IFRS revenue recognition is guided by two primary standards and four general interpretations. GAAP, on the other hand, has highly specific rules and procedures codified for a huge variety of industries on a case-by-case basis. … Under IFRS rules, however, this is prohibited.

What is the key difference between U.S. GAAP and IFRS in relation to the recording process quizlet?

IFRS requires comparative information to be disclosed with respect to the previous period for all amounts presented in the financial statements. US GAAP allows a single year presentation in certain circumstances and SEC rules require two years for the balance sheet and three years for all other statements.

Which is better U.S. GAAP or IFRS?

IFRS enables companies to portray a stronger balance sheet by allowing companies to report the fair market value of assets less accumulated depreciation. GAAP only allows the reporting of cost less accumulated depreciation.What is the difference between U.S. GAAP and IFRS for property plant & equipment?

GAAP includes a provision on how to measure “nonmonetary exchanges” for assets, while IFRS does not. … The cost model must be applied consistently to classes of assets. The revaluation model is very dynamic, but more difficult to use. To use the revaluation model, an entity must be able to determine fair value reliably.

How do IFRS and GAAP differ in their approach to allowing reversals of inventory write downs?

Write Down Reversals GAAP requires that the value of an inventory asset or fixed asset be written down to its market value; GAAP also specifies that the amount of the write-down cannot be reversed if the market value of the asset subsequently increases. Under IFRS, the write-down can be reversed.

What is the difference between GAAP and IFRS Mcq?

IFRSGAAPInternational Financial Reporting StandardGenerally Accepted Accounting PrinciplesDeveloped byInternational Accounting Standard Board (IASB)Financial Accounting Standard Board (FASB)Adopted by

What are the 4 principles of IFRS?

IFRS requires that financial statements be prepared using four basic principles: clarity, relevance, reliability, and comparability.Does US GAAP follow IFRS?

IFRS is used in more than 110 countries around the world, including the EU and many Asian and South American countries. GAAP, on the other hand, is only used in the United States.

What are the US GAAP standards?The specifications of GAAP, which is the standard adopted by the U.S. Securities and Exchange Commission (SEC), include definitions of concepts and principles, as well as industry-specific rules. The purpose of GAAP is to ensure that financial reporting is transparent and consistent from one organization to another.

Article first time published onWhat is the difference between GAAP and US GAAP?

IFRS is a globally adopted method for accounting, while GAAP is exclusively used within the United States. GAAP focuses on research and is rule-based, whereas IFRS looks at the overall patterns and is based on principle. GAAP uses the Last In, First Out (LIFO) method for inventory estimates.

What is difference between IFRS and Indian GAAP?

The key difference between IFRS vs Indian GAAP is that IFRS is the international accounting standards that provide guidance on how different transactions should be reported by the company in their financial statements which is used by many countries, whereas, Indian GAAP are the generally accepted accounting principles …

What is true about US GAAP and IFRS treatment of inventory?

GAAP permits the use of all three of the most common methods for inventory accountability; the IFRS forbids the use of the LIFO method. IFRS requires that inventory is carried at the lower of cost or net realizable value; U.S. GAAP requires that inventory is carried at the lower of cost or market value.

Is hedge accounting mandatory under US GAAP?

Both US GAAP and IFRS permit application of hedge accounting to only certain eligible hedging instruments and hedged items and require formal designation and documentation of a hedging relationship at the beginning of the relationship and an assessment of effectiveness.

Does US GAAP have OCI?

Like US GAAP, the income statement captures most, but not all, revenues, income and expenses. Other items of comprehensive income (OCI) do not flow through profit and loss. … Items of profit and loss and OCI can be presented as: a single statement: the ‘statement of comprehensive income’; or.

How do I convert US GAAP to IFRS?

- Conversion approach.

- Accounting policy.

- Data gaps.

- Conversion adjustments.

- GAAP reconciliation.

- System and process changes.

- Financial reporting.

- Conversion audit.

What is the difference between GAAP and IAS?

GAAP are the more generic accounting rules that every country holds, and are directly influenced by the different accounting boards of each jurisdiction, whereas, IAS is the specific set of internationally recognized accounting standards, set by the IAS Committee.

Is IFRS more conservative than US GAAP?

IFRS firms are more conservative than U.S. GAAP firms.

Why does the US not use IFRS?

As the SEC’s purpose is to protect investors in US companies, especially US investors, they have shown some resistance to the adoption of IFRS. The SEC cites IFRS’s lack of consistency and believes IFRS is underdeveloped when it comes to small-scope issues in reporting.

Does the US use IFRS?

Currently, more than 500 foreign SEC registrants, with a worldwide market capitalisation of US$7 trillion, use IFRS Standards in their US filings. … The IFRS for SMEs Standard is required or permitted. The IFRS for SMEs Standard is neither required nor expressly permitted.

What does GAAP stand for in accounting?

The standards are known collectively as Generally Accepted Accounting Principles—or GAAP. For all organizations, GAAP is based on established concepts, objectives, standards and conventions that have evolved over time to guide how financial statements are prepared and presented.

How does accounting standards differ from accounting principles?

The main difference between Accounting Concepts and Accounting Principles is; Accounting concepts are the assumptions, guidelines, and postulates with which the accounting data is recorded whereas Accounting principles are the rules to be followed while reporting financial data.

How many standards are there in IFRS?

The following is the list of IFRS and IAS issued by the International Accounting Standard Board (IASB) in 2019. In 2019, there are 16 IFRS and 29 IAS.

What are the 10 principles of GAAP?

- Principle of Regularity.

- Principle of Consistency.

- Principle of Sincerity.

- Principle of Permanence of Methods.

- Principle of Non-Compensation.

- Principle of Prudence.

- Principle of Continuity.

- Principle of Periodicity.

What are the 12 GAAP principles?

- Accrual principle. …

- Conservatism principle. …

- Consistency principle. …

- Cost principle. …

- Economic entity principle. …

- Full disclosure principle. …

- Going concern principle. …

- Matching principle.

What are the 4 principles of GAAP PDF?

The four basic constraints associated with GAAP include objectivity, materiality, consistency and prudence.

Which of the following describes a difference between a balance sheet prepared using US GAAP and IFRS accounting standards?

Which of the following describes a difference between a balance sheet prepared using U.S. GAAP and IFRS accounting standards? IFRS balance sheets often report noncurrent items first, although the format is not prescribed. Shareholders’ equity is composed of which of the following accounts?

What is hedge accounting IFRS?

Last updated: 25 May 2020. The objective of hedge accounting is to represent the effect of an entity’s risk management activities that use financial instruments to manage exposures arising from particular risks that could affect P/L or OCI (IFRS 9.6.

What is the difference between hedging and hedge accounting?

A hedge fund is used to lower the risk of overall losses by assuming an offsetting position in relation to a particular security. … The point of hedging a position is to reduce the volatility of the overall portfolio. Hedge accounting has the same effect except that it is used on financial statements.

How is the fair value of a forward contract determined by US GAAP?

The fair value of a foreign currency forward contract is determined by reference to changes in the forward rate over the life of the contract, discounted to the present value.