How much is an HO 6 policy

The average cost of condo insurance, also known as HO-6 insurance, is $429 per year across all 50 states. However, the average cost for this type of policy varies greatly depending on where you live and the amount of coverage you need.

How much does loss assessment coverage cost?

How much does loss assessment coverage cost? A loss assessment coverage endorsement typically costs an extra $25 to $50 a year, which is a small amount to pay to ensure a loss doesn’t leave you financially strapped. Loss assessment coverage limits can range anywhere from $10,000 to as much as $100,000.

Does HO6 replacement cost?

Coverage includes dwelling coverage of $50,000, medical payments coverage of $5,000, contents replacement at replacement value and loss of use at 10 percent of personal property limit.

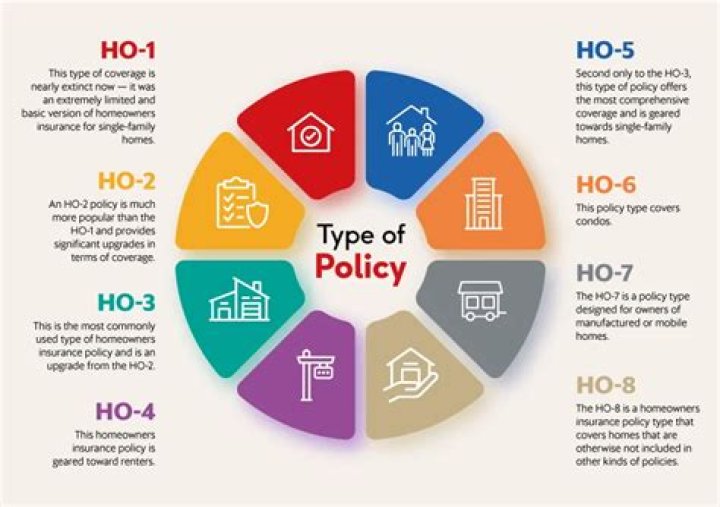

What is an HO 6 policy?

An HO6 insurance policy is homeowners insurance for those who own a condominium or co-op unit. As a condo or co-op unit owner, you own and are likely responsible for damages to your unit. … HO6 condo insurance protects your unit and everything it contains, provides liability coverage, loss of use coverage and more.Is Ho 6 insurance required?

Is condo insurance required? If you have a mortgage on your condo, your lender will typically mandate an HO-6 policy. Additionally, your homeowners or condo association may require certain coverages and limits.

What is the average cost for earthquake insurance?

The average cost of earthquake insurance in the US is $800 per year. Keep in mind that insuring a single-family house in California can cost more — between $1,248 to $2,744 annually for $500,000 of coverage.

Is there a deductible for loss assessment coverage?

There is never a deductible for Loss of Use. Helps pay your share of certain assessments that your owners association may levy on its members to pay for earthquake-damage repairs or a master-insurance-policy deductible. … Deductible options range from 5% to 25% of the Loss Assessment coverage limit.

What is the difference between an HO3 and HO6 policy?

The largest difference between the two types of policies are that an HO3 policy is specifically for a house that is owner occupied and an HO6 policy was created for a condo unit owner. … An HO6 policy will not cover any of the building items outside of your condo unit.Does HO6 cover roof?

HOA policies cover roof damage, but HO-6 policies don’t. If a calamity causes additional damage within your unit, the HOA policy would cover some losses, while your condo policy would cover your personal damage.

Does HO6 cover water damage?Yes, water damage can be covered. Condo insurance covers sudden accidental damage to your property but does not include water damage due to long term causes such as slow leaks.

Article first time published onWhat happens if a condo is destroyed?

When the condominium is declared by the local government as habitable or safe for human use, the homeowners’ association/corporation can decide to repair the destroyed portion of the building, particularly the common areas. The affected condo owner shall repair his/her own condo.

Do I need homeowners insurance for a condo?

Is Condo Insurance Mandatory? Similar to homeowner’s insurance, there is no law that requires condo owners to insure their condo. However, most condo associations and financial lenders require it as part of your contract or mortgage agreement.

Who pays HOA insurance deductible?

2. Benefit of the Coverage. The lower unit that benefited from the association’s insurance pays the deductible.

Is HO6 insurance mandatory in Florida?

While condo insurance, or HO6 insurance, isn’t required by Florida law, your mortgage lender or homeowner’s association likely do require it. Condo insurance not only protects your belongings from damage or destruction, it also includes liability coverage that could protect you if you are sued.

What does an HO4 policy cover?

HO4 insurance, or renters insurance, is financial coverage for 1) damages or losses to your stuff 2) legal fees if you’re sued 3) other’s medical bills if you’re at fault and 4) temp living expenses if your place becomes uninhabitable. Score!

How is dwelling coverage calculated for a condo?

If the square footage of your condo is 1,000, for instance, multiply that number by $100 for a rough estimate of desired condo dwelling coverage. Or, 1,000 x $100 = $100,000 of coverage at a minimum. Both of these condo dwelling coverage calculators provide estimates for needing coverage limits.

How does loss assessment work?

Loss assessment coverage is a policy that works in addition to the HOA policy. It provides protection to condo owners when the building or common areas have been involved in a claim. It covers the remaining out-of-pocket expenses — due to qualifying perils — that weren’t covered under the condo’s HOA policy.

What is loss settlement?

The loss settlement amount is the funds that an insurance company pays out to the homeowner in the event of a homeowner’s insurance claim. In the case of homeowner’s insurance, homeowners are typically required to carry insurance that will cover at least 80 percent of the replacement value of their house.

What is covered under loss of use?

Loss of Use coverage only applies when your home becomes uninhabitable resulting from a covered loss. This coverage covers any Additional Living Expense, meaning any necessary expense that exceeds your normal standard of living. For example, you normally spend $300 per month for groceries.

Is earthquake insurance a good idea?

While earthquake insurance can be great to have if your home is seriously damaged and the damage exceeds your deductible, the high premiums and deductibles that come with earthquake coverage can make the balance between what you pay and what you get uneven.

Why is earthquake insurance so expensive?

Earthquake deductibles are high because the damage from them tends to be catastrophic, making them a higher risk for insurers. To cover costs, they need to make deductibles high.

Is earthquake covered by insurance?

Earthquakes and coverage Homeowners and renters insurance does not cover earthquake damage. A standard policy will, however, generally cover losses from fire following a quake and, if such a fire makes your home unlivable, cover the additional living expenses incurred while you live elsewhere during repairs.

Are windows covered on an HO6 policy?

For example, if a storm breaks a window in your condo, letting rain in to soak your furniture, a condo insurance policy would cover the cost of replacing both the window (structure) and the furniture (personal property). Personal property coverage isn’t limited to things that are located inside the condo unit.

What is Walls in coverage for condos?

Walls In: Also referred to as “single entity coverage” or “studs in” refers to real property coverage from the exterior framing inward, including fixtures. However, this would not include alterations, appliances or other property types contained within the walls of a condo unit.

What does an HO 2 policy cover?

HO2. An HO2 policy is another basic homeowners insurance policy. It covers the 10 perils listed on an HO1 policy, and some additional perils, including falling objects, and weight of snow, sleet, or ice. In total, it covers 16 perils.

Is HO6 a townhouse?

Townhome Insurance is HO6 The most common townhome insurance policy is called the HO6 policy. The HO6 insurance policy was specifically designed for condo and townhome owners where there were shared walls and home owners associations that cover many exterior perils.

What is an HO 10?

Policy Highlights. Included Coverage. Liability – Policyholders are covered if an injury occurs to someone while on their premises, or if they accidentally injure someone or damage property while they are away from the home.

Is condo insurance Same as townhouse?

Key differences in condo vs. In a townhouse, the owner is usually responsible for both the interior and exterior because everything on the land it’s built on is owned by the individual. A condo insurance policy is an HO-6, while townhome insurance is an HO-3.

Is a leaking toilet covered by insurance?

Homeowners insurance may help cover damage caused by leaking plumbing if the leak is sudden and accidental, such as if a washing machine supply hose suddenly breaks or a pipe bursts. … So, if damage results after you fail to repair a leaky toilet, for example, homeowners insurance likely will not pay for repairs.

Is frozen hot tub covered by insurance?

A frozen hot tub may be covered by homeowners insurance depending on what caused the freezing. … Many policies cover “freezing of a plumbing, heating, or air conditioning system.” If your insurer determines that your hot tub connection falls under this protection, they may help you with the damages.

Does insurance cover toilet overflow?

If the toilet overflow is caused by a clogged drain, it is covered by homeowner’s insurance. … If the drain pipes are blocked and the toilet’s flushing system is broken, water can fill up in the pipes and will eventually lead to toilet overflow. Such cases are generally covered by homeowner’s insurance.